There is a proposal, in a draft law that was published on January 13, 2022, for the changing of legislation on a number of issues. We will focus on the denial of significant exemptions for foreign residents regarding residential apartments: tax exemption on rental income, exemption from betterment tax on the sale of a sole apartment, and linear exemption for the betterment of an apartment that is not a sole apartment.

It is stated in the explanatory words to the draft that foreign residents (not including Israelis having an Israeli I.D. card who are no longer residents of Israel), own 83 thousand residential apartments, approximately half of which are located in Tel-Aviv and Jerusalem. In light of the shortage of apartments on the supply side and the high prices, it is being proposed that the tax reliefs that exist for residents of Israel in identical cases be denied to foreign residents, as follows:

Cancellation of an exemption on rental income from residential property for foreign residents

Rental income from residential property in Israel is exempt from tax up to a ceiling of approximately NIS 5,000 (approximately $1,500) a month.

It is proposed that the exemption shall no longer apply for a foreign resident, and from now on a foreign resident can make an election between reporting and having a tax liability on the regular tax track (at the marginal tax rate on the income less expenses and depreciation) and tax at a rate of 10% on turnover (at this stage it is not proposes to deny a foreign resident the election for a 10% tax track).

The application of the proposed change – as from January 1, 2024 and thereafter.

Comment: If the Taxes Authority really has the abovementioned distribution, with the identification of the apartments that are owned by foreign residents, and if the amendment in this matter is passed as is, it will be interesting to see whether 83,000 people will actually be added to the number of submitters of reports and payers of taxes (less any double counting for foreign residents who own several apartments)!

Cancellation of the exemption for a foreign resident on the sale of a sole apartment

Real (non-inflationary) betterment on the sale of a sole residential apartment up to a sale value of approximately NIS 4.5 million is exempt from betterment tax at present.

A foreign resident must prove (there are ways that make this easier) that it is their sole residential apartment, in other words, he does not have another apartment in his country of residence).

It is proposed that this exemption be cancelled for a foreign resident, and that it will only apply to a resident of Israel.

The application of the proposed change – it is proposed that the new law shall apply to the sale of a residential department that is executed as from January 1, 2024 and thereafter.

Qualification for an exemption: It is proposed that the new law shall apply to a resident of Israel who becomes a foreign resident, if and only if on the day on which the apartment is sold five years have passed since the day on which he ceased to be a resident of Israel.

Cancellation of an exemption for a foreign resident on the sale of an apartment that is not a sole apartment (the linear exemption)

“The linear exemption” – the sale of a residential apartment, which is not a sole apartment, is currently chargeable with taxation in accordance with the “linear exemption”, i.e.: the capital gain is divided into two periods:

The component from the day on which the apartment was purchased and until the end of the year 2013 is tax exempt;

The component beginning in 2014 and up to the day on which the apartment is sold – chargeable with betterment tax at a rate of 25%;

The application of the proposed change – on the sale of a residential apartment that is executed from January 1, 2024 and thereafter.

It is proposed that this exemption be also denied to foreign residents and that is will only apply to a resident of Israel

Insights regarding a foreign resident

The legislator is seeking to signal a red light warning to foreign residents, that it is worth their while to get rid of the residential apartments that they own, and that they should realize the profits that they have generated from them – and that this is certainly the case if they are sole apartments, and even if they are not such, they still contain a significant linearly exempt component – up to January 1, 2024!!!

We would mention that the transfer of an apartment from a foreign resident to a resident of Israel as a gift without consideration, is an appropriate solution in the relevant circumstances.

The crypto industry forms part of the Hi-tech industrial sector, and in this industry too it is generally acceptable to find crypto based remuneration for someone who is connected to a project, similarly to share based remuneration or employees’ stock options. Thus, for example, if a project in the industry includes within its framework the issuance of a cryptographic currency/token, it is very often found that the currencies are granted to the project’s employees, to service providers and to entrepreneurs.

Whereas with employees’ shares or stock options, it is customary to make use of Section 102 of the Israeli Tax Ordinance (taxation profits as capital gains, subject to conditions and to Tax Authorities’ approval), the section does not apply where we are dealing with remuneration in the form of a token. A partial solution can be found in a professional circular, which has been published by the Tax Authority in Israel (the number of which is 7/2018) which deals with the issuance of crypto currencies (ICO), where it is determined that the employee’s income will be chargeable with taxation at the earlier of the time of the exercise of the right that is inherent in the token, or at the time of its sale. The classification of the income is as income from work or a business.

An additional alternative that the Tax Authority permits a company to elect for is the taxation of the employee at the time of the allocation of the tokens to the employees, whereas at the time of the actual sale of the token by the employee, tax will apply in accordance with its status (capital gain or salary income). It should be mentioned that where a company has made such an election, it will have an allowable expense in accordance with the amount of the income that has been determined to be income from salary in the hands of the employee. This is similar to the allowance of an expense under Section 102 for a company that has elected for the “regular income track” rather than the “capital gains track”.

Complex tax questions arise in the field of remuneration of those involved in crypto projects and the following is a description of some of them:

How should an entrepreneur who “keeps” cryptocurrency currencies “for himself” be treated? Is this a dividend? And what if there is no company in the project and the activity is performed “independently”? Is it possible to claim that this is the “building of an asset” by the entrepreneurs? Is this business income in the entrepreneurs’ hands?

Remuneration in the hands of providers of services for crypto consideration – here in our opinion, the answer is less complicated, which is because it is customary that the consideration, or at least part of it, will be deemed to be business income. The Tax Authority relates to this issue in a tax decision that was issued to our office (the number of which is 209/18): “The manner of the recording of receipts that are received in cryptocurrencies” – the decision deals with service providers where the receipt in their hands is a “cryptocurrency” and it deals with aspects relating to reporting and recording by the service providers.

The question of the deduction of tax at source – creates greater complexity in light of the Authority’s position that a cryptographic currency is an “asset”, and where the issue is one of an exchange of assets (“exit” to bitcoin or to any “stable currency” whatsoever, such as USDT for example), the issue is far more complex.

Locked-up cryptocurrencies – what are the rules regarding grants that are received in the form of currencies for which a “lock up period” applies? In a case in which an evaluation is required – such evaluation is not simple to perform in light of the lock up period and the tremendous fluctuations in this field. And if we need to “add some spice” to the stew – in the lock up period it is possible to retain the coins or alternatively to deposit them in a yield-bearing instrument – “Staking” etc.

The determination of a value for the currency – the circular published by the Tax Authority related to an average value in the 30 trading days after the tax event. We would mention here that there is no always trading in these currencies and therefore the “solution” regarding the determination of the value is not always efficient.

As we can perceive, the field of cryptographic currencies is far more complex than the basic questions – is it a “currency” or an “asset”. The industry is changing and developing at great speed and the Tax Authority cannot relate to every trend in the field. Our firm accompanies crypto entrepreneurs and investors and we have considerable experience in providing consultancy services in this complex and fascinating field.

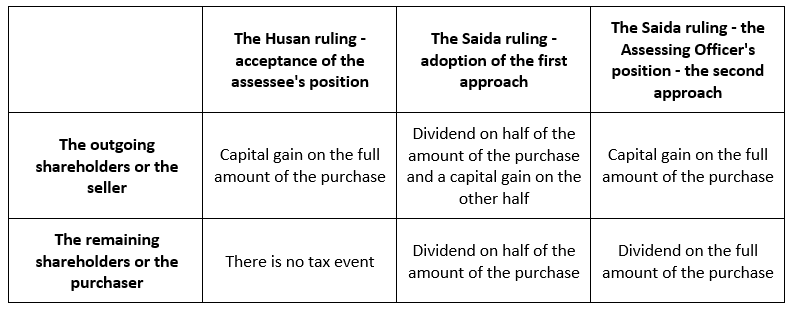

In this newsletter, we will be examining the subject of self-purchase from the perspective of international taxation following the recent case law on the subject in Israel. The ruling by the District Court on the Beit Husan case, Tax Appeal 71455-12-18 on November 5, 2020, permits companies to execute self-purchases, where there is a business reason for the transaction, without the need to cope with the tax implications regarding the taxation of notional income or the classification of income from the sale of shares by a foreign resident as a capital gain (which in most cases is exempt from tax in Israel under the force of the internal law or the provisions of the tax treaty) or as a dividend, for which tax must be deducted at source.

On September 26, 2021 a ruling was handed down in the case of Meir Saida 38294-02-19, which dealt yet again with the question of the tax liability of shareholders in a self-purchase transaction.

The Tax Authority’s position on the issue of self-purchase

The tax aspects regarding a self-purchase were determined in a circular that was published by the Tax Authority (Number 2/2018): where a company purchases its shares from all of the shareholders, proportionately, the purchase will be viewed as the distribution of a dividend, whereas on a self-purchase other than “pro-rata”, the two following approaches are calculated:

The first approach: The purchase will be viewed firstly as the distribution of a dividend to all of the shareholders (those remaining and the seller) in accordance with their shares before the self-purchase, and afterwards it will be viewed as if the remaining shareholders had purchased the shares from the selling shareholders. In other words, part of the amount that has been received by the seller will be classified as a dividend and an additional part will be classified as a capital gain.

The second approach: First, the remaining shareholders will be viewed as if they have purchased the shares from the selling shareholders, in the amount of the purchase in accordance with their relative shares in the Company. Afterwards, they will be viewed as if the remaining/ purchasing shareholders have transferred the shares that they purchased to the Company, in consideration for the amount of the purchase in an exchange transaction, such that a dividend will arise for them at the level of the amount of the purchase. The Tax Authority’s position is that this approach is to be adopted primarily where the selling shareholders have sold all of their shares in the company and afterwards, they have not holdings at all in the Company and indeed this is the approach that the Assessing Officer sought to implement in the Saida case.

The ruling in the Saida case

The Court determined that there is a significant difference in the facts between the Husan case and the Saida case and it adopted specifically the first approach in the Income Tax circular, as described above.

The following table summarizes the rulings by the District Court and the approach adopted by the Income Tax Department from the perspective of the remaining shareholders and the selling shareholders:

It arises from an analysis of the tax events in the table that the classification of a remaining shareholder’s income or that of the purchaser (in the event that a tax event has occurred) will be dividend income and the classification of the selling or outgoing shareholder will be classified as a capital gain or as a dividend or as a combination of the two.

The implications of the different classification for the outgoing or selling shareholders

In the event that the income is classified as a capital gain – the difference between the consideration and the shares’ cost will be taxes as a capital gain. If it is classified as a dividend – the full amount of the dividend will be taxed and the Company will be required to deduct tax at source.

In the event that the outgoing shareholder is a foreign resident individual

The classification of his income as a dividend will be taxed, generally at a rate of 25%/ 30% with the addition of surtax, or at a lower rate if he is a resident of a country with which Israel has a tax treaty.

The classification of the income as a capital gain and not as a dividend may, however, increase the tax rate in certain circumstances (the marginal tax rate in a linear calculation up to the determining time (January 1, 2003) however it may also result in a full exemption being given if the provisions of Section 97(B2) or 97(B3) of the Israeli Tax Ordinance are met, and in a treaty country, the exemption is usually granted and may even be broader.

In this connection, it can be mentioned that in certain circumstances, there may be a claim both in respect of a remaining shareholder and in respect of an outgoing shareholder that part of the consideration on the self-purchase, which is classified as a dividend pursuant to the provisions of the internal law, is to be classified as a capital gain pursuant to the provisions of the treaty.

In the event that the Company executing the self-purchase is foreign resident

A new immigrant, a returning veteran resident and a returning resident will benefit from a tax exemption on a dividend for a period of 5 to 10 years in accordance with their status, whereas for a capital gain, the exemption is for a period of 10 years and a partial tax exemption will be given for the period thereafter.

If the outgoing/ selling shareholder is a company that is resident in Israel, the classification of the income as a capital gain and not as a dividend will negate the possibility of receiving an indirect tax credit (in contrast to the dividend approach).

To summarize, the ruling brings up the issued that engage in a self-purchase event yet again. However, let’s remember that this is a ruling by the District Court. Until there is a final ruling, it is expected that uncertainty will be there regarding this issue, and we would recommend that each case should be examined thoroughly, in accordance with the specific circumstances.